Reports

2024 > 08

Per Johansson and Oscar Severinsson join Origo Fonder

Origo Fonder is pleased to announce the appointment of Per Johansson as the new Co-Chief Investment Officer (Co-CIO). Per brings with him a proven track record of over 20 years in the industry, having consistently delivered top-tier performance in both rising and declining markets. His extensive experience includes serving as a fund manager and analyst at Fidelity in London and Boston for 11 years, as well as founding and acting as Chief Investment Officer (CIO) of the award-winning hedge fund Bodenholm and Boden Capital. Most recently, Per was a Partner at D&G. In addition to his new role, he will become a shareholder in Origo Fonder, starting his new position in September.

Simultaneously, Origo Fonder has appointed Oscar Severinsson as the new Chief Operating Officer (COO). Oscar’s background includes positions at Skandia and Catella Funds, where he served as Head of Fund Operations. Most recently, he was a business developer at ISEC. Throughout his career, Oscar has developed a broad expertise in areas such as fund administration, risk control, compliance, and reporting.

Stefan Roos, Founder and CIO of Origo Fonder, comments:

"Per is a unique stock-picker whom I've been following since he launched the hedge fund Bodenholm. He was undoubtedly our most impressive industry colleague and competitor. I thought then, 'If you

can't beat him, partner with him.' Now, several years later, everything has fallen into place. With Per's recruitment, we are adding an exceptionally skilled manager and analyst to our team. Per has demonstrated an ability to generate long-term alpha regardless of market conditions. Together, I see us as one of the more experienced teams in genuinely active Nordic equity management. We are very pleased to have Per joining the firm both as a partner and manager. Origo has grown over recent years and launched another small-cap strategy, and with Per on board, we are now ready to take the next step together. We are also pleased to welcome Oscar as our new COO. Oscar’s drive and background in data-driven fund administration and regulatory issues will be invaluable as Origo takes its next step forward."

Per Johansson comments:

"I have known Stefan for a long time and have followed Origo's strong performance from the side. The development of the fund over the past 12 years, both in the hedge fund and in the long leg's alpha, I consider to be world-class. When Stefan shared his vision for Origo, I immediately knew I wanted to be a part of it. I am very enthusiastic about Origo’s funds and future, and I believe we complement each other well. Together, we can deliver very good risk-adjusted performance and interesting products for our investors and partners."

About Origo Fonder:

Origo Fonder is an independent fund management company (AIF manager) under the supervision of the Swedish Financial Supervisory Authority since 2012. The team specializes in investing in listed small-cap companies in the Nordic region and manages the multi-award-winning hedge fund ORIGO QUEST, as well as the recently launched focused small-cap fund ORIGO SELEQT. The investment philosophy is based on a pure small/mid-cap focus, with active constructive ownership in sustainable business models. The client base consists of international and Nordic institutions, foundations, and private individuals.

• Origo Quest has a low-beta strategy focusing on absolute returns. Quest has been nominated three times as the best smaller European hedge fund by HFM and has achieved ~9% annual returns since its inception in 2013.

• Origo Seleqt is a long-only fund with high market exposure, distinguished from traditional small-cap funds by being concentrated, genuinely Nordic-focused, and focused on true small-cap companies.

* Please see www.origofonder.se for more information.

Contact: stefan.roos@origofonder.se

Press release PDF

Risk information: Past performance does not guarantee future performance. The value of your investment may rise as well as fall and there is no guarantee you will recover your original investment. An investment in Origo Quest or Origo Seleqt should be seen as a long-term investment.

Rotation into the small cap segment

• Weak macro figures and increased hopes for interest rate cuts

• Interest in small companies continued to increase

• Invested more in undervalued gem

Global equities started strongly but lost momentum during the month, closing at -0.5%. The conflict between Israel and Palestine went wrong, weak economic figures from China and nervousness around the Q2 reports contributed to profit taking. In general, we saw pressure on last year's large-cap winners at the same time as buying interest in the small-cap segment increased. In the US, the Russell 2000 small-cap index rose by 11.1%, while the S&P 500 rose only 0.9%.

The rotation into small caps is the theme of the summer and is primarily driven by hopes for future interest rate cuts combined with relatively attractive valuations. In addition, we see increased M&A activity and that small companies are clear targets in these processes.

The Nordic stock markets went in different directions, but here too, small companies and companies with low valuation multiples ("value companies") had a better development. The Nordic small company index rose 3.8% during the month. The gap with the large companies is still large, with the small company index lagging behind by around 30% in the last two years. We are at the end of the second quarter reporting period and so far the positive deviations are slightly outweighed, but it took a really good report to impress the market.

One of our insights from several company and macro reports is that Germany looks weak. Germany, which has long been dependent on Russian gas, is also the EU's largest exporter to China, with exports twice as high as the EU average. A strong dependence on Russia and China contributes to pressure their industry. Given the relatively high valuation of several industrial companies in the Nordics and their exposure to Germany, this is a risk that we have tried to manage.

Profoto's quarterly report turned out much as we had expected. Turnover increased by 7% to SEK 196m, of which organic growth accounted for the entire rise. Several product launches drove the increase, while the general demand from photo studios and e-commerce customers remained on hold. Profitability weakened and the operating margin fell to 18.5% (25.8), which, however, is still a level that many similar companies can only dream of. Interesting in the report is the CEO's speech, where it is made clear that the company's strong investment in innovation and focus on more product launches is fixed. We expect that these product innovations will begin to be felt in the income statement during Q4 and above all during 2025.

Profoto is a typical Origo company with high gross margins, good cash flow and a leading niche position, while the company is undervalued. A real gem. The stock has been under pressure in 2023/2024 in the wake of high interest rates and tepid consumption, but we believe macro conditions are turning and growth will pick up. We have increased the holdings in our funds during the month.

The service company Coor delivered a worse report. Again, we may unfortunately add. The operating margin of 5.1% and an underlying growth of -1% do not impress. Individual quarters can always be affected by special events, but in Coor's case, the mediocre development has unfortunately been a trend in recent years. Our investment thesis in 2018 was based on a belief that the stable cash flow would generate acquisitions, which in turn would lead to above-GDP growth and rising profitability. We have been wrong in our analysis and have gradually divested our holding during 2023/2024.

Husqvarna (short position in Quest) presented a shaky report where weak weather conditions and generally weak consumption led to sales growth of -6%. The company writes that market conditions are still tough, which is certainly true, but in our analysis we also assume that Husqvarna has structural challenges. We assess that Husqvarna's position with dealers has weakened in the last 3-5 years and that the transition from a petrol-based product range to electric drive is one of the explanations. Too low a percentage of direct sales and rental are other challenges, and in addition, the company seems to have fallen behind when it comes to the new generation of chain-free robotic lawnmowers. We have had a short position on and off in Husqvarna in recent years and the report essentially confirms our thesis.

Our funds have developed strongly over the past 24 months. Origo Quest, our absolute oriented hedge fund has delivered 9.3% while the correlation (Beta 24m) amounts to a moderate 0.45. Quest has been well paid for the company analysis and generated positive returns in both the long and short books. In percentage terms, the short book has actually delivered the best, which is quite interesting given that the market has risen by 20% during the period. The low-beta strategy means that investors get exposure in a fund that is not particularly dependent on the market trend, and that you get an asset whose movements deviate from the rest of the portfolio. The annual return, which since its inception 12 years ago amounts to 8.6%, is created with significantly lower market risk than a traditional equity fund.

Origo Seleqt, our concentrated micro/small company fund has returned 21.6% in the last 24 months, which is in line with the fund's benchmark (VINX Small Cap SEK NI). At the same time, we can state that the fund has performed significantly better than most similar funds and is currently 10-15 percentage points better than the median value of the fund category. The micro/small company segment has developed worse than the large company segment in recent years, and the valuation difference is large. It is our firm opinion that the valuation of the fund's holdings does not reflect a long-term "fair value".

ORIGO QUEST

Origo Quest returned 0.4% for the month, which means 3.4% so far this year and 158% since inception. The long book had a positive development, while the short gave a somewhat negative return. The long/short spread thus became positive. In the long book, it was primarily Freetrailer, Addtech and SparNord that accounted for the largest positive contributions. Addtech delivered a Q2 report well above market expectations, achieving a record margin of 15.3% leading to a 25% gain. Husqvarna fell sharply and contributed positively to the monthly return, while the reverse happened in NCC. During the month, we took the opportunity to increase Alm. Brand, which we financed with increased short sales.

ORIGO SELEQT

Origo Seleqt rose by 1.0% during July. The benchmark index VINX Small Cap rose at the same time by 3.8%. Since the beginning of the year, the return amounts to 17.3%, which is in line with the index. Addlife, SparNord and Freetrailer provided the best return contribution. Europris, VBG and Protector made negative contributions. Alm.Brand recently sold its Energy division and announced that the proceeds will be returned to the shareholders. At the same time, they took the opportunity to raise several of their financial targets. The sale of the energy part is an important piece of the puzzle in our investment case, but the most important thing is that the synergies from the purchase of Codan are realized. During the month, we have, among other things, increased Alm. Brand and sold ATEA

/Team Origo

Strong first half of the year

- Strong half-year - but a mixed stock market

- Elekta below our expectations

- New investment in opportunistic property company

The small companies rebounded after a period of very strong development and the Nordic small company index lost 2.3% during the month, which means an increase of 13.0% since the beginning of the year. Swedish small companies, where the real estate sector weighs heavily, have not kept up with the rest of the Nordic region and are up by 8%.

Recently, the market's enormous focus on inflation and interest rates has decreased somewhat and we see signs that the companies' fundamental development has become an important factor. This suggests that the "small company revenge" since March will continue. It should not be forgotten that the small companies, which deliver better profit growth over time, underperformed on the stock market in 2021, 2022 and 2023. Four years of underperformance relative to the large companies is historically extremely unusual.

Elekta (-19% YTD) came up with a weak quarterly report during the month. Both organic growth and margins were lower than expected and also lower than what the company had guided for before the report. After five straight quarters of improvement, management says the quarter was challenging with a number of installations taking longer than planned which had a negative impact on revenue and profit. We do not know if it is some installations that are the real problem, but rather see opportunities for improvement in terms of governance and internal follow-up. Elekta operates in an attractive growth market and now has a modern and strong product portfolio including the recently launched AI-powered EVOaccelerator. Despite that, Elekta has so far had inexplicably difficulty in raising profitability.

The management's ambition is to lift the gross margin of 37% to the levels before the pandemic, when it was 42%. We believe that the potential is clearly higher than that and really see no reason why Elekta's margin should be up to 10 percentage points (our assessment) lower than the main competitor Variance. The management must now show that you can get a return on all the investments you have made in the last five years and that efficiency is increasing. In addition, there are good opportunities for the important Chinese market to gain momentum and for the new and strategically important collaboration with GE Healthcare to start yielding returns. We expect earnings growth of around 30% for this year and next while the stock is valued at 12X operating earnings. Good risk/reward in a high-tech growth company with a strong global market position.

Spar Nord Bank rose 8% during the month (+25% YTD) after once again raising its earnings forecast. Our investment thesis almost three years ago was based on the fact that we saw a good opportunity for significant distribution of capital to the shareholders given the company's strong balance sheet and good credit quality. We note that the company's development fully follows our plan. We expect rising returns on capital again this year, a new internal IRB model for calculating how much capital the bank must hold to cover its risks and high dividends and buybacks.

SLP, Swedish Logistic Property, is a new holding in our funds. The company's strategy is to acquire and develop logistics properties primarily in southern Sweden. The company is relatively new (2018 and listed on the stock market in 2022) but has already demonstrated a good ability to make value-creating purchases of properties in a niche that we have followed closely since our investments in Tribona and Catena about 10 years ago. The Q1 report was strong and earnings (CEPS) rose to 0.43 (0.38) driven by higher rents and improved net financials. We think the stock is undervalued and that "small is beautiful" in a capital-intensive industry that is coming back to life after the inflation and interest rate shock of 2022-2023. It will be particularly interesting to follow the sector's development going forward. We see several global signals (destocking is in its final phase, manufacturing is moving home, new investments in infrastructure, the energy transition is accelerating, the inflation problem is soon a thing of the past) that may play out so that the manufacturing industry and cyclical consumer goods receive support.

The division of the stock market, as it has looked in the last 4-5 years, may then be close to the end of the road.

ORIGO QUEST

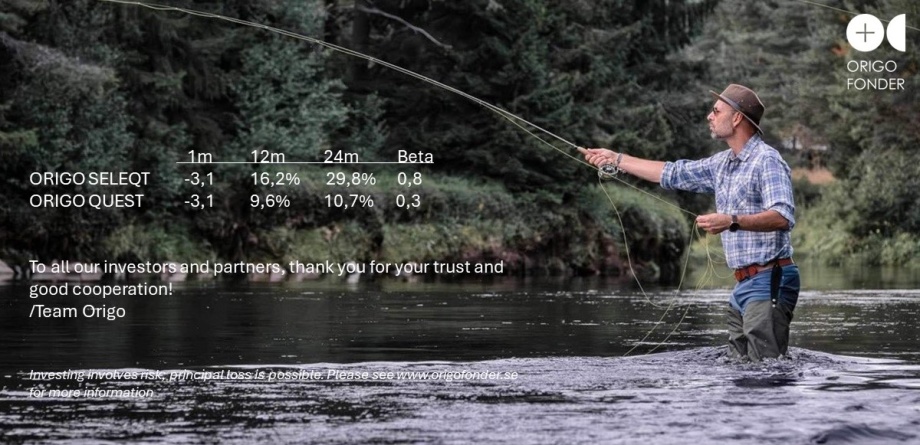

Origo Quest lost 3.1% in June, giving 3.0% YTD and 9.6% on a rolling 12 month basis. The long book had a weak development (eg Elekta) while the short book (eg RVRC) gave a positive return. The long/short spread was overall negative. Since the start, the return amounts to 157%, which corresponds to 8.6% per year.

The fund is positioned to have low correlation to the stock market and 24m Beta amounts to 0.3. The net exposure amounted to 55%. MTG, Elekta and RaySearch are major long-term investments during the year. The card book is currently focused around companies with significant accounting, value creation and valuation risks.

ORIGO SELEQT

Origo Seleqt lost 3.1% in June after the strong rise in March-May. The return during the first half of the year was thus 16.2%, just over 3 percentage points better than the benchmark index. Elekta accounted for a large part of the negative deviation during the month. The software company BIMobject, a smaller holding in the fund contributed well after a positive analysis in the newspaper Affärsvärlden.

The fund is concentrated and currently consists of of roughly 30 real small caps, where the majority have a market cap between SEK 500 million and SEK 20 million. Elekta, New Wave and MTG are the fund's largest investments during the year. Nekkar and Trifork have been sold.

We also want to take the opportunity to thank all our investors for your trust and good cooperation during the first half of the year and wish you a really nice summer!

/Team Origo